How does Furro work?

Furro runs on a community model, where pet owners share unexpected treatment costs together. It's a more affordable alternative to traditional pet insurance, built on a different structure than an insurance company.

How does Furro work?

Furro runs on a community model, where pet owners share unexpected treatment costs together. It's a more affordable alternative to traditional pet insurance, built on a different structure than an insurance company.

Furro in brief

Furro was born from the idea of bringing the way early village communities helped one another into the modern age — supported by technology. We believe traditional insurance companies do a lot of good. At the same time, we believe a community model can be a more affordable, fairer and more practical option, especially for pet owners.

Furro is a community of pet owners where members share vet costs among themselves. Joining takes only a moment, monthly fees are charged to your card, and getting treatment works without extra hassle. In practice, the outcome is familiar: your pet gets care, you pay part of it, and the community covers the rest.

Joining

Joining happens through the price calculator: enter your pet's basic details and you'll see a price estimate right away. If your pet has been healthy, you can usually activate Furro in just a few minutes.

Joining

Joining happens through the price calculator: enter your pet's basic details and you'll see a price estimate right away. If your pet has been healthy, you can usually activate Furro in just a few minutes.

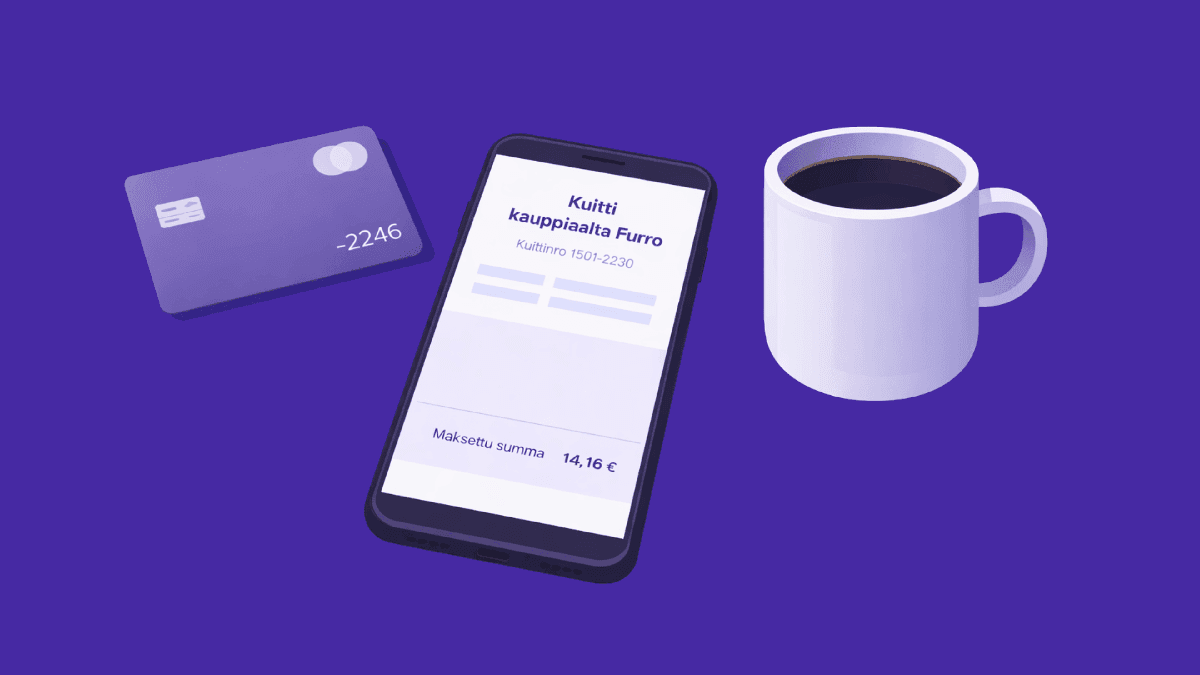

Paying

With traditional insurance, the premium is usually paid in advance for the whole policy period. With Furro, the monthly share is easily charged to your card once a month, based on the community's actual costs. Watch the Finnish video at the bottom of this page to see how Furro's billing works in practice.

Paying

With traditional insurance, the premium is usually paid in advance for the whole policy period. With Furro, the monthly share is easily charged to your card once a month, based on the community's actual costs. Watch the Finnish video at the bottom of this page to see how Furro's billing works in practice.

Getting treatment

When your pet needs help, find a Furro partner clinic using the clinic search on our site. In exceptional cases, you can also seek treatment at other clinics.

Getting treatment

When your pet needs help, find a Furro partner clinic using the clinic search on our site. In exceptional cases, you can also seek treatment at other clinics.

A fast direct-settlement model

AI brings speed to the process at direct-settlement clinics. Furro's direct-settlement model is built on collaboration between AI and clinics. At direct-settlement clinics, costs can often be handled within a few minutes during the visit, at any time of day or night.

A fast direct-settlement model

AI brings speed to the process at direct-settlement clinics. Furro's direct-settlement model is built on collaboration between AI and clinics. At direct-settlement clinics, costs can often be handled within a few minutes during the visit, at any time of day or night.

What makes Furro unique?

Furro isn't just a more affordable alternative to pet insurance — it works in a structurally different way. These three principles explain where the difference comes from.

The community's funds go to treatment

Furro doesn't use the community's funds for its own business; instead they go directly to caring for pets. Community members pay a small fixed membership fee for the upkeep of the platform.

Furro optimises for fairness

The models Furro builds start from the goal of treating cases as fairly as possible. The AI model helps ensure that cases are assessed consistently, evenhandedly and in line with the Community Rules.

We're on the same side of the table

At Furro, the setup is different from traditional insurance models. Furro doesn't benefit from reducing the costs handled within the community at members' expense. Furro's and the members' goals are therefore aligned: fair and consistent assessment, an honest way of operating, and smooth, reliable access to care for pets.

How do the community's funds stay sufficient?

We want every member to understand how the community's funds cover treatment costs. That's why we explain the cost-sharing model transparently.

Furro's model is designed so that the community's funds are estimated to be enough to cover treatment costs with over 99.8 percent probability at the level of any single month. The estimate is based on actuarial modelling that accounts for the probability distribution of treatment cases, cost variation and the buffer.

The price cap is a buffer

The community typically uses about a third of its maximum collection capacity. The remaining two thirds are an unused buffer.

The size of the community helps

Furro's community has grown to a level where the impact of individual large treatment costs on the whole is smaller than before. The community's growth improves predictability and consistency.

Is it possible that the funds wouldn't be enough?

The probability of that is very small, under 0.2 %. In practice it would mean an exceptional crisis that multiplied treatment costs across the entire community. Relying on a mathematical model is a deliberate structural choice at Furro.

How is Furro different from pet insurance?

Furro meets the same basic need — being prepared for unexpected vet costs — but in a different way than a traditional insurance company. Here are the biggest differences.

Pricing

An insurance company's pricing is based on risk analysis, costs and profit targets. The premium typically stays the same throughout the policy term, regardless of whether any claims occur.

With Furro, a member's monthly share is based on the community's actual treatment costs and varies from month to month, a bit like spot-priced electricity. On top of this, a membership fee of 6 € / mo is collected. All in all, the cost settles at roughly half the level of traditional pet insurance.

Cash flow

At an insurance company, premiums are the company's income, which it uses to pay claims, cover its own costs and invest those funds.

With Furro, the community's funds are collected into the community account at the turn of the month, from where they are passed on to clinics or to members who have requested cost sharing. Furro doesn't use the community's funds for its own business.

Financial responsibility

In traditional insurance, the financial responsibility is carried by the insurance company, which has statutory obligations to pay claims.

With Furro, the financial responsibility lies with the peer community — in practice, with the members together. Furro provides the technology platform but doesn't carry the financial responsibility for treatment costs and doesn't act as an insurance company.

Payment guarantee and consumer protection

An insurance company guarantees the payment of claims with its solvency capital, and the policyholder is protected by insurance legislation and oversight from the Finnish Financial Supervisory Authority.

Furro doesn't provide an insurance-company-style guarantee, but the price-cap buffer model ensures with over 99.8 percent certainty that the community's funds are enough to cover costs. It's important to understand, however, that Furro's members don't have the traditional consumer protection based on insurance legislation. Members' rights and obligations are determined by the membership agreement and the Community Rules.

What would Furro have cost for your pet?

Choose your pet's breed and age to see what your monthly share would have been with Furro over the last 3 months.

Join us (Finnish)What would Furro have cost for your pet?

Choose your pet's breed and age to see what your monthly share would have been with Furro over the last 3 months.

Our mission is to fight the rising costs in the pet care industry

Caring for and insuring pets has become significantly more expensive in recent years, leaving many of our four-legged friends without protection.

Watch the Finnish video to see how Furro works in practice.

Our mission is to fight the rising costs in the pet care industry

Caring for and insuring pets has become significantly more expensive in recent years, leaving many of our four-legged friends without protection.

Watch the Finnish video to see how Furro works in practice.

Frequently asked questions

Furro isn't an insurance company or an insurance policy. Furro is a modern alternative to traditional dog and cat insurance. It's a Finnish community of pet owners that runs on a peer-to-peer cover model, where vet costs are shared together according to agreed rules. Furro is operated by the Finnish company FairShare Technologies Oy, which provides the technical platform and the rules, but the financial responsibility for treatment costs lies with the community's members among themselves. As a member, your monthly fee is determined by the actual, rules-based treatment costs that arise, and it can range between 6 euros and a personal price cap. As a general rule, over the long term Furro costs around half as much as traditional pet insurance. Furro's mission is to make caring for and protecting pets affordable, transparent and fair.

As a Furro member, you have the right to request a reimbursement when it concerns your pet's illness or accident, and when your pet has no specific exclusion or waiting period for the matter. In practice this means that when your pet falls ill or gets injured, a Furro direct-settlement clinic or an approved clinic treats your pet according to its own medical judgement, and the Furro community contributes to the treatment costs according to pre-agreed ground rules. Typically Furro covers, for example, vet appointments and emergency visits, examinations such as blood tests, X-rays and ultrasound, procedures and surgeries along with the related anaesthesia, hospital care and monitoring, medication, and the supplies and materials directly related to treatment. In addition, follow-up checks belonging to the same course of treatment can be shared within the community within the limits of the Community Rules. Coverage is affected by your chosen level of cover (Basic or Plus), the limitations defined in the Community Rules such as any waiting periods, age limits and per-treatment maximums, and whether the situation is an excluded one. Not all vet costs are eligible for sharing: the Community Rules separately describe the exclusions (for example certain preventive procedures, vaccinations, or illnesses that began before joining). What Furro does not cover Furro doesn't cover every vet cost. The exclusions are based on the peer community's shared rules, and their purpose is to keep the ground rules predictable and the sharing of costs fair for all members. Typical exclusions are preventive care and “healthy animal” visits, such as vaccinations, routine check-ups and deworming, as well as most ordinary dental care when it isn't clearly the treatment of an illness or accident. In addition, illnesses or ailments that began before membership are typically subject to limitations, and some structural problems or breed-specific risk factors may come with separate limitations in the Community Rules. Furro's cover also generally doesn't include non-medical incidental costs or support services, nor over-the-counter products or feeds beyond very limited cases, if at all. Emergency surcharges may be limited in situations where the visit wasn't medically an emergency by the definition in the Community Rules. It's worth checking the precise terms and exclusions in the Community Rules before joining, or asking the site's AI bot about what's covered.

Furro suits dog and cat owners who want an alternative to traditional pet insurance and who value affordability, fairness and transparency. With Furro you don't pay a fixed insurance premium in advance; instead, you contribute to the peer community's actual, rules-based vet costs. Your monthly fee can range between six euros and the personal price cap defined for your pet, meaning your own maximum liability is capped. Furro is a natural fit for you if you accept the basic idea of the peer model: the financial responsibility for treatment costs is borne by the community, not an insurance company. In terms of a smooth experience, the biggest benefit is seen at direct-settlement clinics, where a reimbursement recommendation for sharing the costs is produced quickly as part of the clinic's normal process, so there's no separate back-and-forth over a reimbursement application. If, on the other hand, what you specifically want is an insurance contract with an insurance company, a fully predictable fixed price, or for the liability for reimbursements to always lie with the company, traditional pet insurance may suit you better.

Furro is for dog and cat owners who want to share vet costs in a peer community instead of taking out traditional insurance. Membership is open to any natural person who creates a user account and applies for membership, accepts Furro's Terms of Use, the membership agreement and the peer community's rules, adds at least one dog or cat to the service, and adds a payment card from which the monthly shares can be charged. The pet must meet the peer community's eligibility requirements. In practice these may mean, for example, age limits, waiting periods or other individual restrictions. When joining, the pet's state of health and previous illnesses must be reported truthfully, because they affect what the community can share at any given time under the rules. The exact terms are set out in the Community Rules, so that you know in advance the conditions under which you and your pet can join Furro.

If you're switching to Furro from an old pet insurance policy, time the change so that your old insurance is still in force through Furro's waiting periods. At Furro the waiting period is 10 days for accidents and 30 days for illnesses from the start of membership. For certain predefined groups of illnesses the waiting period is 120 days. This reduces the risk of a gap during which your pet has no cover at all. It's worth noting that illnesses that begin during the waiting period are generally not shared by the community, and they may later lead to limitations. That's why symptoms and ailments appearing during the waiting period should be treated and documented as normal, but be prepared for the fact that they aren't within Furro's scope. If an accident occurs or an illness or symptoms appear during the waiting period, the pet owner should reassess the overall picture of whether it's wise to keep the old insurance in force for now, or even remain a customer of it. Ailments that begin during the waiting period are usually not shared by the Furro community, and they may lead to limitations. That's why it's important to weigh the situation case by case: if the symptoms involve further examinations, courses of treatment or monitoring, keeping the old insurance in force can be a sensible way to ensure coverage and continuity of care. A short overlapping period between the old insurance and Furro helps reduce the risk of the pet or owner falling “between the cracks” when it comes to reimbursements, and it often also reduces surprises and disappointments. Waiting periods exist because they benefit the whole community by keeping the model fair for everyone.

When you need help, the primary and smoothest option is to go to a Furro direct-settlement clinic or an approved clinic. You'll find clinics near you in the Clinic search on the website or in Oma Furro. At direct-settlement clinics, the clinic submits the visit details to Furro, so the cost-sharing gets a Community Rules-based assessment as part of the normal treatment process. Typically you pay only your own share and any non-covered items at the till, and the portion eligible under the Community Rules is routed for sharing within the peer community. At an approved clinic, you pay for the visit yourself as normal and request a reimbursement afterwards. In exceptional situations, you can seek care at any clinic. In that case you pay for the treatment yourself first and request a reimbursement afterwards. Exceptional situations include: - There's no direct-settlement clinic or approved clinic within a 50 km radius - The direct-settlement clinic or approved clinic doesn't offer the required treatment - The direct-settlement clinic or approved clinic isn't open in an urgent situation - It's a life-threatening emergency for your pet In emergencies, your pet's health always comes first. If it's a life-threatening situation or sudden severe symptoms, primarily seek care at the nearest Furro direct-settlement clinic or approved clinic, or if none is available, the nearest emergency vet, even if it isn't a direct-settlement clinic or approved clinic. Once the situation is under control, you can submit the visit details to Furro afterwards so the case can be processed according to the Community Rules. If you otherwise need advice or support If you have questions about your own membership, pricing, reimbursements or the Community Rules, you can first ask the site's chatbot about your matter. You can also always get in touch with Furro support at hei@furro.com. In short: in an acute situation you contact a vet first; for all other questions, the Furro chatbot or Furro support by email.

Peer-to-peer cover is a modern way to protect what you own, and it means a model in which people in a similar situation share costs with each other according to jointly agreed rules. Instead of a traditional insurance company, protection arises from community members contributing to one another's eligible costs as they come up. Around the world, peer-to-peer cover is growing strongly, and the same development is now under way in Europe too. The model has become especially common in consumer products such as pets, electronics and vehicles, where speed and transparency stand out. In the peer-to-peer cover model, the funds collected from the community go as they are toward covering costs, without the costs of middlemen or a traditional insurance company. In addition, as a community member you get to see what the money is used for, the costs are clearly itemised, and the model rewards fair conduct and prevention in a way that lets every community member come out ahead. At Furro this shows up in the fact that you don't pay a fixed insurance premium in advance; instead, your monthly fee is determined by how much rules-based vet cost has arisen in the community during that month. Your own maximum monthly liability is capped by the personal price cap defined for your pet, which is based on the pet's risk profile. When you visit a direct-settlement clinic, the clinic can check via Furro on a case-by-case basis whether the costs can be shared under the Community Rules. AI supports this interpretation by giving a reimbursement recommendation, and you usually pay only the deductible at the visit. The rest, i.e. the portion eligible for sharing under the rules, is allocated to the community, and the monthly shares are charged on the first day of the following month via the payment processor. While Furro provides protection for your pet similar to traditional insurance, it's good to note that Furro isn't an insurance company nor traditional insurance. Furro is a technology platform and operating model that enables cost-sharing within the community, and the financial responsibility for the costs to be shared lies with the peer community within the limits of the Community Rules.

Furro is a peer-to-peer cover-based way to cover the treatment costs arising from your pet's illness or accidents. Furro and traditional pet insurance solve the same problem, namely the unpredictability of vet costs, but they do it differently. Furro isn't an insurance policy issued by an insurance company; it's a peer community of pet owners in which costs are shared according to the community's rules. The model In peer-to-peer cover, all the funds collected from the community go as they are toward the treatment costs of community members, which makes the pet owner's monthly fees significantly more affordable. In addition, avoiding unnecessary examinations and treatments that aren't in the pet's interest lowers the prices of the whole community's peer-to-peer cover. In this way, every fair choice made by each member and vet collectively affects everyone's fees and thus encourages all parties to act fairly and correctly. Who bears the risk In traditional insurance, the insurance company is liable for reimbursements when the terms are met. At Furro, the financial responsibility is borne by the peer community, i.e. the members among themselves. FairShare Technologies Oy, which operates behind Furro, provides the technology platform and the process, but doesn't act as an insurance company and doesn't pay treatment costs from its own balance sheet. How the price is formed With insurance you usually pay an agreed premium in advance. At Furro you don't pay a fixed premium in advance; instead, each month you contribute to the community's actual, rules-based treatment costs. Your monthly share can range between 6 euros and the personal price cap defined for your pet. How things work at the vet clinic In the traditional model, reimbursements are often requested afterwards and processing can take time. At Furro the benefit is seen especially at direct-settlement clinics: the clinic checks via Furro whether the costs can be shared and AI gives a recommendation based on the Community Rules, so you pay only the deductible at the visit and the rest is brought to the community for sharing. If you go somewhere other than a direct-settlement clinic, you pay for the treatment yourself first and submit the patient records for assessment afterwards. Transparency A significant difference from traditional pet insurance is that community members get to see clearly what the fees cover and on what ground rules the community operates. The peer-to-peer cover model will give community members a clear view of where pet owners' monthly fees are used. Consumer protection and contracts Because Furro isn't insurance, it doesn't involve the same statutory structures and liability for reimbursement as the insurance-company model. At Furro, rights and obligations are determined by the Terms of Use, the membership agreement and the Community Rules, which are worth reviewing with regard to limitations and what's covered. In the Furro model, members don't have traditional consumer protection available to them.